Summary

- PPG Industries is an industry leader, providing paints and coatings to consumers and industries around the world.

- The company has felt the impacts of COVID-19, as demands from the aerospace and automotive industries have dropped off.

- In this article, I intend to analyze the company from a technical and fundamental perspective, and make a recommendation.

When I think about the types of companies that Warren Buffett likes to invest in, I’m often reminded of companies with business models that are easy to understand. These types of companies are typically ones that even a sixth-grader can appreciate and comprehend. There is a lot of beauty in the simple, easy-to-understand business models of these types of companies that are less likely to be disrupted by technological innovation. However, just because a business model is easy to understand doesn’t mean that it is immune from economic cycles, as is the case with many manufacturing companies.

I believe the company that I have for you today, PPG Industries (PPG), fits that mold. In this article, I intend to evaluate the company from different angles and make a recommendation, so let’s get started.

(Source: Fortune)

A Global Company With A Focused Business

PPG Industries is a global manufacturer of paints, coatings, and specialty materials. It is a Fortune 200 company with headquarters in Pittsburgh, and has operations in nearly 70 countries worldwide. The company was founded more than 130 years ago as a plate glass factory, and started its coating business in 1900. It operates two business segments, with performance coatings comprising 60% of sales, and industrial coatings making up the remaining 40% of sales. Its performance segment supplies coatings for architecture and aerospace, while the industrials segment supplies coatings for automotive, packaging, and industrial equipment.

What I like about PPG industries is that it essentially sits in a manufacturing sweet spot in that its cost structure is not as capital-intensive as companies like Boeing (BA), where a drop in demand causes supply chain issues, and not so capital-light that it opens the door for too much competition. To supplement its growth and to enhance its moat, PPG has made a number of acquisitions to enhance coatings technologies that it did not already have. This enables the company to scale production of these new technologies across its global facilities.

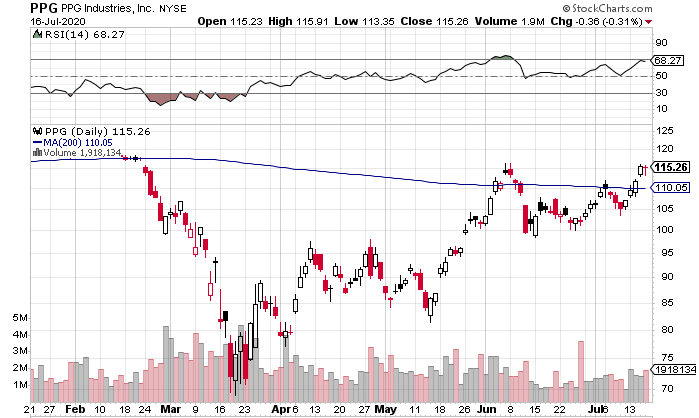

Turning to the stock price performance, the stock has had a solid recovery since hitting lows in March. At present, it is sitting above its 200-day moving average of $110 and has an RSI of 68, which indicates that the share price gains have been somewhat over-extended into overbought territory.

(Source: StockCharts)

Looking into the financials, today, PPG reported Q2 results, which surprised the investment community in that the results were not as bad as anticipated, driven by increased do-it-yourself demand for the company’s home paint products in all major regions. However, the company has shown its sensitivity to economic cycles as net sales were down by about 25% versus Q2’19, due to the global weakness that was brought upon by COVID-19.

The performance coating segment saw a 15% YoY decline, which was driven by a 30% decline in aerospace coatings volume. Industrial Coatings saw an even bigger decline, with a 40% YoY drop in net sales. This was driven by a nearly 50% YoY drop in automotive coatings volume, due to substantial cutbacks in global automotive production.